- Compare agents

- Online valuation

- Explore my area

- Home toolkit

- News & guides

- Estate agents by area

- Sold house prices by area

- Estate Agent ValuationRequest an in-person valuation with an agent to discover your property's true market value.

- Online Valuation ToolGet a free instant estimate of your home's value.

- EPC CheckerFind out if your home has a valid Energy Performance Certificate.

- Listing MonitorAlready on the market? See how your online property advert is performing.

- Selling guides

- Estate agent guides

- Mortgage advice

- Conveyancing guides

- Property news See All News & Guides

Agent shortlist

HouseWorth

Estimated reading time: 18 minutes

Table of contents

- 1. Is it better to go with a fixed or variable rate mortgage?

- 2. Fixed rate mortgage

- 3. Tracker mortgage

- 4. Fixed vs tracker mortgage

- 5. Alternatives to fixed and tracker mortgages

- 6. Help with getting a mortgage

- 7. How long should you get a mortgage for?

- 8. Are tracker mortgages cheaper than fixed?

- 9. Is it better to fix your mortgage for two or five years?

- 10. Is it worth paying off my mortgage early?

- 11. Summary: Undecided? Hire a mortgage broker

If you're hoping to land your first mortgage, or are looking to remortgage in the near future, it's shaping up to be a tough ride. The question for many homeowners is simple: which mortgage package should I choose?

In this article, we dig deep into market specs and give you some much-needed answers, as well as some alternatives to fixed mortgages and trackers. But first, let's tackle the big question head-on.

In the UK we are typically faced with a choice of two types of mortgage: a fixed rate package or a variable rate like a tracker. But which is better?

Is it better to go with a fixed or variable rate mortgage?

Fixed or tracker, two-year or five-year - the specifics of the best mortgage for you are not in black and white. For some homeowners, a two-year fixed mortgage may be the best choice, while a lifetime tracker might be better for others.

To find out the right mortgage package, you need to work out a number of things, including:

1. Your personal finances

There's no surprise that how much you can actually afford to spend has a big impact on the type of mortgage you should get. Can you afford the higher rates of a fixed mortgage? Or does the prospect of rising base rates detract from the attractiveness of a tracker?

2. Your plans for the years ahead

The mortgage you pick needs to work for you - and that means timings. For instance, if you're thinking of moving in the next two years, it would be ludicrous to lock in a five-year fixed rate. Unless you can port your mortgage for a low fee, you'd have to remortgage and fork out for an Early Repayment Charge, which could cost a small fortune.

3. The mortgage market

Ultimately, you've got to compare available deals to find the one that meets both your needs and affordability. Many changes in the mortgage market depend on the Bank of England base rate. Interest rates of both fixed rate and trackers fluctuate according to the base rate.

4. Your appetite for risk

The primary difference between fixed and tracker mortgages is this: on the one hand, you have a package with a locked-in rate of interest, and on the other, you have a package that tracks the Bank of England's base rate.

So when we talk about fixed and tracker mortgages, we’re talking about security vs risk - but we're also talking about immobility vs opportunity. A fixed rate deal might be more secure, but you'll benefit immediately from rate cuts with a tracker.

So how do I know what's right for me?

You need to carefully consider your options. You can get a good start on this by:

- Assessing your current finances.

- Planning for the years ahead.

- Researching available mortgages.

- Weighing up what you can afford to pay for and what you can't.

To help you along the way, we've done our research into the UK's biggest mortgages.

To give you a basic idea of what you're dealing with, we've stripped these mortgage deals down to their bare essentials:

Fixed rate mortgage

A fixed rate mortgage is a mortgage with a static interest rate. Interest rates of available fixed rate deals fluctuate with the ups and downs of the market. Once you lock in a fixed deal however, your interest rate is fixed for the length of time outlined in the deal.

Fixed rate features:

- Fixed repayment each month with rate of interest pre-determined for a number of years.

- When interest rates are low, your fixed deal remains the same, but new fix deals change accordingly.

- When interest rates rise, the best fixed fee packages (those with low interest rates) dry up fast.

- Fixed mortgages tend to have higher interest rates than trackers, but you pay more for the security.

- When your fixed rate mortgage ends, you switch to the lender's Standard Variable Rate (SVR).

- If you overpay or leave your fixed rate early, you'll incur an ERC which can be 1 - 5% of your outstanding mortgage.

What do you pay with a fixed rate mortgage?

You pay a fixed fee each month (dependent on the size of the mortgage you take out) with interest pre-determined for a number of years. When interest rates rise, the best fixed fee packages (those with lower rates) dry up fast.

How long are fixed rate mortgages?

The most common packages are two, four, and five year rate fixes but they can be longer.

What happens at the end of a fixed rate mortgage?

When a fixed rate deal ends, your mortgage automatically switches to the lender's SVR. This is the lender’s standard base rate, and unlike a tracker, it changes according to the lender's whim - which can make it an expensive alternative.

Why choose a fixed rate mortgage?

People tend to choose fixed rate mortgages for security - you usually pay higher interest than trackers but the amount you pay stays the same no matter what. With a tracker on the other hand, you're playing a bit of a gamble by relying on interest rates remaining low. A fixed, however, provides certainty.

If you know money is going to be tight, knowing the exact cost of your month to month repayments can be a big help. Or, if rates are currently low, it might be worth locking them in with a fixed deal.

Why you shouldn't choose a fixed rate deal

Fixed rate mortgages may sound attractive, especially while interest rates are low. But you need to think carefully before making such a big financial commitment. You'll be locked into your deal for several years at best because most deals have Early Repayment Charges - charges you have to pay if you leave your agreement early or overpay your mortgage.

When is the best time to choose a fixed rate deal?

There isn't really a best time, but some people prefer to lock in a fixed rate while rates are low so they can benefit for the long run.

![]()

Tracker mortgage

A tracker mortgage is a type of a variable rate mortgage. This means its rate of interest goes up and down according to an external source like the Bank of England (BOE) or the London Inter-Bank Offered Rate (LIBOR). Where a tracker mortgage differs from a SVR, is that it directly tracks the external source, whereas a SVR changes whenever the lender decides to adjust it.

Tracker mortgage features:

- Variable-rate mortgage, meaning that your monthly repayments can go up and down according to an external interest rate like the Bank of England or LIBOR.

- Some trackers are fitted with caps or collars. These can either limit the amount of interest you pay (saving you money if the BOE's base rate goes through the roof), or prevent you from paying too little (preventing you from taking advantage of extremely low rates).

- More predictable than SVRs because SVRs change to the whim of the lender, whereas trackers track an external rate.

- Common durations are five years or lifetimes. With a lifetime tracker, you’re locked in for the entirety of your mortgage.

- Trackers let you play the market. They are the opposite of fixed where you pay for security.

- When a tracker ends, you'll switch to the lender's Standard Variable Rate (SVR).

- If you overpay or leave your tracker early, you'll incur an ERC which can be 1 - 5% of your outstanding mortgage.

What do you pay with a tracker deal?

Like a fixed rate, you make mortgage repayments each month, but because your rate of interest changes with the Bank of England base rate, you might be paying more (or less) some months than others.

Changes to your tracker's interest rate are unpredictable. No one truly knows which way the market is going, or how the BOE's base rate will change.

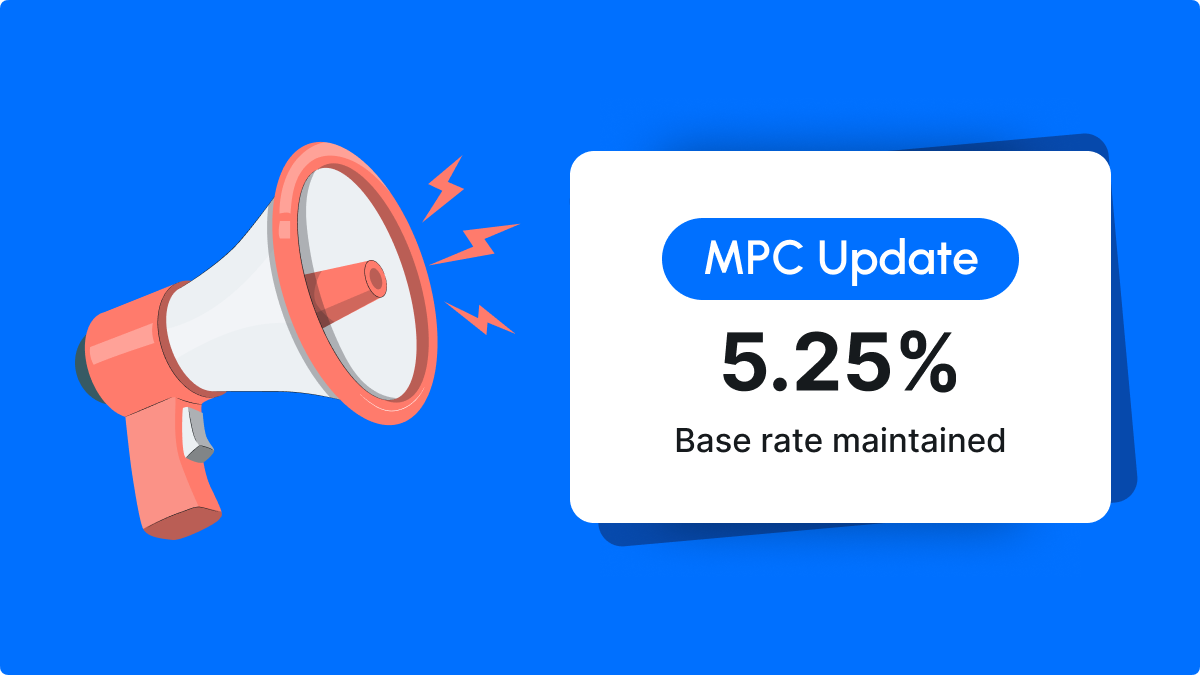

In recent history, changes to the BOE's base rate have been infrequent. For decades, the UK has enjoyed remarkably low interest rates - until now.

How long is a tracker mortgage?

As with fixed rate deals, the length of a tracker can vary. You can find 2-year and 5-year trackers, and you can even get a lifetime tracker - a deal that lasts for the duration of your mortgage.

It's worth noting that the longer a tracker lasts, the higher the interest rate will sit above the BOE's base rate.

What happens at the end of a tracker deal?

Unless you're on a lifetime tracker (which concludes at the end of your mortgage) you will be moved onto your lender's SVR. As a result, your monthly payments will likely increase.

Why choose a tracker deal?

Unlike a static, fixed rate mortgage deal, a tracker offers borrowers a chance to take advantage of fluctuating interest rates. Your monthly repayments will closely follow the Bank of England base rate, meaning you might be able to save money when rates go low.

Not only do you have an opportunity to save with a tracker, but you also gain some transparency. Your mortgage's rate of interest moves in line with the state of the economy, not to the whims of lenders.

Why you shouldn't choose a tracker deal

The sheer level of unpredictability associated with a tracker mortgage can be a big turn-off for borrowers. If the base rate goes up, you will be spending more money without actually clearing your mortgage debt.

What's more, some trackers do come with collars and caps, which can prevent you from making the most from extremely low interest rates.

When is the best time to choose a tracker deal?

Until recently, the UK has enjoyed low interest rates. Because of this, trackers have been fairly popular. You can take advantage of low rates with immediate effect.

But at times where rates are higher, a tracker mortgage can be a much more attractive proposition. As rate cuts become an increasing possibility, you will stand to benefit from lower interest rates immediately, unlike those stuck on fixed mortgages.

It takes 2 minutes.

Fixed vs tracker mortgage

Let's take a deep dive into the pros and cons of both mortgages. What might make a fixed mortgage better for you than a tracker, or vice versa?

What are the advantages of a fixed rate mortgage?

- You know exactly what you're paying month to month with a pre-determined interest rate locked in for a duration agreed between you and your mortgage lender.

- Knowledge of your monthly outgoings may make it easier to budget and plan your life.

- If rates begin to increase, you can take solace in the fact that your rate will remain the same.

- If you remortgage or apply for a mortgage while rates are low, you may be able to lock in a cheap fixed rate deal.

What are the disadvantages of a fixed rate mortgage?

- Being locked into a deal with fixed repayments, especially if your interest rate is high, can be very frustrating - especially if rates are reducing.

- Early Repayment Charges can be expensive, making both remortgaging and moving home costly affairs.

- After your fixed rate concludes, you will switch to the lender's SVR. This can be very expensive, so you'll need to line up a new mortgage in time.

What are the advantages of a tracker mortgage?

- When interest rates are low, a tracker mortgage can be extremely advantageous. With your tracker rate following a base rate like the BOE's, you can immediately benefit from low rates.

- With reduced tie-in periods, trackers can be much more flexible than fixed rate mortgages.

- If you lock in a tracker mortgage while rates are high, you may be able to benefit from 'inevitable' rate reductions.

- When rates are low, tracker deals are generally cheaper than fixed rate deals.

What are the disadvantages of a tracker mortgage?

- If the base rate increases, so will your monthly repayments. As no one can really predict when the base rate will increase or not, this creates a good deal of uncertainty.

- Some tracker mortgages come with collars which prevent their interest rates from going below a certain level. This can prevent you from making any real benefit from being on a tracker.

- As with a fixed rate mortgage, when a tracker reaches its conclusion, you'll transfer to your lender's expensive SVR.

- Similarly to a fixed rate, ERCs are handed out to those who exceed mortgage overpayments or remortgage too early.

Alternatives to fixed and tracker mortgages

There are other types of mortgage packages available, but they aren't as popular as the big two. Here are a couple of them:

Standard variable rate mortgage (SVR)

As we've mentioned throughout the article, every mortgage lender has an SVR - a variable rate mortgage that follows the Bank of England's base rate, but changes according to the lender's whims. SVRs tend to be more expensive than trackers and fixed rates, but they are more flexible.

With most SVRs, you aren't locked in. There are no Early Repayment Charges to pay, meaning you can move to another mortgage as and when you please.

Why is this useful? Well, if you're in the middle of big life events or changes, moving to an SVR can be a good way to bridge the gap between mortgages.

There are also low arrangement fees, which can be an attractive prospect if you're worried about the thought of remortgaging in the near future.

Discounted variable rate mortgage

Banks and building societies sometimes offer variable rates at a discount, with lower rates than their SVRs. The discounted period usually lasts for a short duration (up to three years), after which your rate switches back to the SVR.

With most discounted variable rate mortgages, you are locked in for a specific length of time. But at a discounted rate, ERCs tend to be smaller, making it easier to overpay or remortgage.

Please note that if the SVR is low already, discounted rates won't be as competitive. And don't forget, if the BOE's base rate increases, so will yours. While discounted, it's still a variable rate mortgage.

Help with getting a mortgage

If you’re worried about your affordability, there are ways you can increase your buying power, especially if you were planning to buy alone. Let’s take a look at joint and guarantor mortgages.

Joint mortgages

When working couples purchase a property together, they often take out a joint mortgage. This is an agreement where the two homeowners are jointly liable for the mortgage debt.

It’s not just limited to couples though - many close friends and family decide to purchase property together, especially in expensive areas where getting on the ladder is all the more difficult.

The most common form of joint ownership is joint tenancy. A joint tenancy doesn’t have a quantifiable level of stake - meaning if the owners were to split up, it would be up to the courts to divy up the value.

The other form of joint ownership is tenants in common. Tenants in common each own a percentage stake in the property. So in a couple, each partner would own a 50% share in the house.

Remember: Regardless of the type of joint ownership, the lender maintains the right to pursue either of you for the outstanding mortgage debt.

Is it worth buying with a friend?

Buying with a friend or family member can be a great idea for hopeful homebuyers who aren’t in relationships but want to get on the property ladder - but this venture is a huge commitment and one that shouldn’t be taken lightly.

When you buy with a friend, both your credit scores are taken into consideration, meaning that you can be brought down by your friend’s negative credit score. A rejection will be marked on both your applications. What’s more, a friendship can easily be strained when finances are involved.

Another thing to consider is future prospects. While you both may be happy to live together for a number of years, life can be very unpredictable. If either of you end up in a relationship, an early end to your joint ownership may be on the cards - this can result in an early sale that could cause problems.

Guarantor mortgages

If you’re unable to get the mortgage you need from a lender, you may be able to finance your home purchase with a guarantor mortgage. A guarantor is someone who will make the necessary monthly repayments if you fail to do so. They could be a wealthy family member or sponsor.

So does this mean the guarantor owns your property? No, your name is the only one on the title deeds, but the guarantor will sign a separate agreement with the mortgage lender.

As one can imagine, guarantor mortgages can be a risky business, especially if you are in unstable employment. If you and your guarantor fail to make payments, the mortgage provider is within their right to pursue both you and your guarantor for full repayment. They can force your guarantor to sell their house to make good on your mortgage.

If you’re thinking about getting a guarantor mortgage, make sure you speak to your would-be guarantor carefully so they understand exactly what they are enlisting themselves to. Furthermore, always talk to a mortgage broker to get the best advice on how to proceed - it may be that a guarantor mortgage is avoidable.

How long should you get a mortgage for?

The terms for your mortgage deal, including its length, should always be made in respect of your future plans and finances. Ultimately the market is unpredictable, so while it's worth keeping an eye on the news, you should always pick a mortgage term that works for your specific situation.

Try to work out whether certainty or flexibility is more important to your situation. Typically, the longer you fix your mortgage for, the more this security will cost. However, this is not always the case - according to recent data by Moneyfacts (October 2022), homeowners are now paying more when fixing for two years than they are for five years.

Sometimes, certain deals come with distinct benefits. Some longer deals, like a thirty year mortgage, can come with unlimited overpayments - a bonus that could prove useful if you're expecting an increase to your salary, or already have good savings. With no ERCs to pay on overpayment, you could lower your LTV much quicker than standard.

Are tracker mortgages cheaper than fixed?

Tracker mortgages tend to offer a lower initial interest rate than equivalent fixed term deals - but this is not always the case. Moreover, some trackers are fixed with collars that prevent their rates from reducing below a certain percentage. This can prevent some borrowers from benefiting from extremely low rates.

Is it better to fix your mortgage for two or five years?

It depends on both your financial circumstances and plans for the future. If you're in need of financial certainty, then a five year mortgage might be best. On the other hand, if you'd prefer more flexibility, a two year might be better.

Is it worth paying off my mortgage early?

Yes, living in a house you own can make a massive difference to your life by reducing a great deal of stress and financial worry. But homeowners should always prioritise paying off any debts they owe before beginning to overpay their mortgage.

Summary: Undecided? Hire a mortgage broker

There’s only so much you can do to prepare for mortgages. While it’s perfectly sensible to do your research, there’s no use agonising over every decision you make! Our advice is simple: if you’re unsure about which package to go with, or simply need some advice, hire a mortgage broker to help you make the best decision possible.

Thinking about

selling your home?

Picking the right estate agent is vital for a successful sale. GetAgent makes choosing simple. Discover the best performing agents in your area.

- Free

- Data-driven

- No obligation

Thinking about

selling your home?

Picking the right estate agent is vital for a successful sale. GetAgent makes choosing simple. Discover the best performing agents in your area.

- Free

- Data-driven

- No obligation

Compare estate agents

It takes 2 minutes.

Get in touch

020 3608 6556

Our lines are closed

We are a company registered in England & Wales, company number 09428979.

Copyright © 2026 GetAgent Limited