- Compare agents

- Online valuation

- Explore my area

- Home toolkit

- News & guides

- Estate agents by area

- Sold house prices by area

- Estate Agent ValuationRequest an in-person valuation with an agent to discover your property's true market value.

- Online Valuation ToolGet a free instant estimate of your home's value.

- EPC CheckerFind out if your home has a valid Energy Performance Certificate.

- Listing MonitorAlready on the market? See how your online property advert is performing.

- Selling guides

- Estate agent guides

- Mortgage advice

- Conveyancing guides

- Property news See All News & Guides

Agent shortlist

HouseWorth

Table of contents

- 1. Analyse the latest property prices

- 2. Calculate your mortgage affordability

- 3. Browse available mortgages

- 4. Create a savings plan

- 5. Lifetime ISA (Individual Savings Account)

- 6. Shared ownership scheme

- 7. Help to Buy scheme

- 8. Struggling to pay your monthly mortgage payments?

- 9. Summary: You have options!

For most mortgages, you need a deposit of at least 10% (and usually higher). For a £300,000 house, that’s at least £30,000.

When you factor in estate agency fees, conveyancing costs, Stamp Duty, and moving costs on top of the deposit, it's clear that you'll need a significant amount of cash on hand to make the purchase.

So how do you know if you can afford to buy a house? How can you ensure you are ready to make the big step?

1. Analyse the latest property prices

If you've got an idea of where you want to live, and the type of property you want to live in, the first thing you need to do is find out the value of your ideal home. Zoopla and Rightmove are the most popular property portals in the UK. You can use their websites or apps to browse the latest 'For Sale' properties in different parts of the country.

2. Calculate your mortgage affordability

First time buyers can use a mortgage affordability calculator to work out whether they can afford the loan they need to purchase the property and make subsequent monthly mortgage repayments. You can use the mortgage calculator at MoneySavingExpert or, popular mortgage lender, Nationwide.

Remember: Mortgage affordability is more than just how much money you have in at any one time. Your credit report plays a huge role in your attractiveness to lenders as a borrower. That's why lenders consult an independent credit reference agency, like Equifax, Experian or TransUnion to determine the quality of your credit report. Also, lenders nearly always require bank statements to analyse your annual income and build a better picture of your financial profile.

3. Browse available mortgages

Armed with the knowledge of your mortgage affordability, browse the latest available mortgages on sites like MoneySuperMarket and Comparethemarket. There are different types of deals to choose from, with self-employed mortgages for those in individual employment, and shared ownership mortgages for those seeking a novel, cheaper way of getting on the property ladder.

Pay close attention to interest rates. For at least the first few years with a mortgage, you'll primarily be paying off interest with your monthly repayments. As your Loan-to-Value ratio increases, you'll be able to access better deals with lower interest rates.

Generally, the lower the interest rate, the better the deal - but this depends on your priorities.

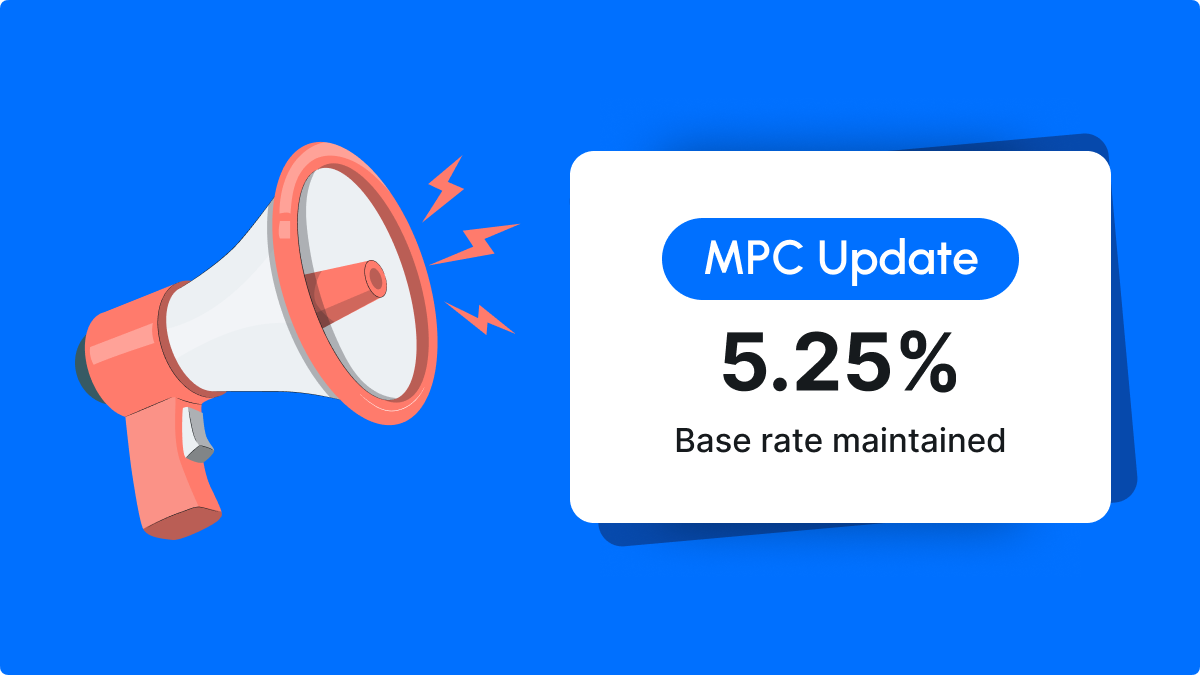

Sadly, your Loan-to-Value ratio isn't the only determiner of mortgage interest rates. The pace at which average interest rates rise is dictated by the state of the economy. In recent history, interest rate rises have frequently made the headlines. You can read more about interest rates in our Property News section.

If you don't have large savings, you may still be able to get a mortgage. Depending on your situation, a government scheme may be able to help.

Create a savings plan

If you don't have enough money to purchase your first home, you need to start saving. Depending on how much you need to save, it might be worth creating a savings plan.

To do this, you need to take all of your ingoings and outgoings into account - almost to a cellular level. Everything you spend from week to week needs to be accounted for.

Once you have tracked your monthly monetary transactions, your next job is to work out where it is viable to make savings without massively denting the quality of your life.

You can devise a savings plan yourself or you can hire an independent financial advisor to do the job for you.

Lifetime ISA (Individual Savings Account)

Lifetime ISAs are a good option, whether you're looking to buy your first home or save for the future. To open a Lifetime ISA, you should be 18 or older but under 40.

How does it work?

You can contribute up to £4,000 each year until you turn 50, with the government adding a generous 25% bonus to your savings, capped at a maximum of £1,000 per year.

It's worth noting that the £4,000 you put into your Lifetime ISA counts towards your annual ISA limit, which is £20,000 for the 2023 to 2024 tax year.

Lifetime ISAs offer the flexibility to hold cash or invest in stocks and shares, or even go for a combination of both.

When you hit 50 years of age, you won't be able to make any more contributions or receive the 25% bonus. However, your account will stay open, and your savings will continue to earn interest or investment returns.

Shared ownership scheme

Shared ownership schemes are a good opportunity to get on the property ladder if you can't afford to buy a home outright.

To be eligible for the scheme, you usually need to have a certain level of household income and be a first-time buyer, or a previous homeowner who can't afford to buy again.

How do shared ownership schemes work?

You purchase a share of a property from a housing association (usually between 25% to 75% of the property's value) and pay rent on the remaining share. Eventually, you can increase your ownership over time through a process called "staircasing."

Shared ownership allows you to enjoy the perks of owning a home while easing the financial burden. Plus, it's a stepping stone towards full homeownership.

Help to Buy scheme

The Help to Buy scheme is designed to help first-time buyers and existing homeowners get onto or move up the property ladder.

How does the Help to Buy scheme work?

With the Help to Buy Equity Loan, the government lends you up to 20% (or 40% in London) of the home's cost if you're buying a new-build property. You'll need to contribute a 5% deposit, and the remaining 75% (or 55% in London) is covered by a mortgage from a lender.

There's no need to worry about interest on the government loan for the first five years. This means you can focus on settling in and managing your mortgage. After the initial five-year interest-free period ends, you'll start paying interest on the loan.

It's worth bearing in mind that there are specific price caps and eligibility criteria for the scheme, so it's a good idea to check the details and consult with relevant authorities to see if Help to Buy is the perfect fit for you.

Struggling to pay your monthly mortgage payments?

On the 14th of July 2023, the Government introduced a Mortgage Charter to help those with mortgage loans during a cost of living crisis. The charter gives borrowers more flexibility in the event of being unable to pay their mortgages.

If you’re struggling financially and are unable to make your mortgage payments, be proactive and communicate with your lender. Consistent late payments will negatively affect your credit score, but your lender should be able to offer you some refinancing options.

A riskier approach would be to investigate an interest-only mortgage plan. This will significantly reduce your monthly payments, but you’ll have to pay the original amount in full at the end of the mortgage term.

Only look into switching to an interest-only mortgage if you’re confident that you’ll be able to save enough to make up the final lump sum. You’ll have to provide a convincing investment plan to a lender on application too.

If you're unsure, talk to an independent financial adviser. They will be able to provide help tailored to your personal situation, and be able to guide you through your options.

Summary: You have options!

Unless you're extremely lucky, buying a house is probably one of the most expensive things you'll ever do. While the task may feel like an insurmountable one, it's reassuring to know that there are still options if you're struggling.

If you can afford to buy a house, you can begin to get the ball rolling. Explore available properties, check the latest mortgage deals, and begin scheduling house viewings. Here's some questions to ask at your first house viewing.

Thinking about

selling your home?

Picking the right estate agent is vital for a successful sale. GetAgent makes choosing simple. Discover the best performing agents in your area.

- Free

- Data-driven

- No obligation

Thinking about

selling your home?

Picking the right estate agent is vital for a successful sale. GetAgent makes choosing simple. Discover the best performing agents in your area.

- Free

- Data-driven

- No obligation

Compare estate agents

It takes 2 minutes.

Get in touch

020 3608 6556

Our lines are closed

We are a company registered in England & Wales, company number 09428979.

Copyright © 2026 GetAgent Limited