- Compare agents

- Online valuation

- Explore my area

- Home toolkit

- News & guides

- Estate agents by area

- Sold house prices by area

- Estate Agent ValuationRequest an in-person valuation with an agent to discover your property's true market value.

- Online Valuation ToolGet a free instant estimate of your home's value.

- EPC CheckerFind out if your home has a valid Energy Performance Certificate.

- Listing MonitorAlready on the market? See how your online property advert is performing.

- Selling guides

- Estate agent guides

- Mortgage advice

- Conveyancing guides

- Property news See All News & Guides

Agent shortlist

HouseWorth

Estimated reading time: 5 minutes

Welcome to the GetAgent Property Market Update! We've gathered insights from top experts across the UK to keep you up-to-date with the latest market trends.

Despite the continued rise of properties for sale, market growth has been sluggish in April, with both buyer demand and sales numbers still in a state of recovery. However, this abundance of available properties is providing homemovers with plenty of options.

In terms of house prices, April has been a slow month. Although Halifax, Zoopla, and Nationwide have reported minor changes to their average price records, there hasn't been a significant shift in either direction.

Cautiousness is evident among homesellers. According to Rightmove, new listers have only raised their prices by 0.2%, which is significantly lower than the usual 1.2% hike at this time of year.

Stay tuned for more news on mortgages and first-time buyers in this week's property update.

Market continues slow progress to recovery

Although Zoopla predicts at least one million home sales by the end of the year, market recovery has been slow. Despite some regions performing better than others within emerging hyper-localised markets, buyer demand remains low this month.

According to Rightmove, the market's slow recovery is a sign that new sellers are both cautious of economic headwinds, and aware of the market's transition to a slower pace.

House prices remain inscrutable

This month, Halifax reported a slight decrease in the average property price to £286,896, down from £287,880 the previous month.

However, Nationwide reported a 0.5% increase in house prices in April after seven consecutive months of decline, with the average property now worth £260,441. Robert Gardner, the building society’s chief economist, suggests that this signals a ‘stabilisation’ of house price growth, but conflicting data from other sources makes it difficult to confirm this. For example, Zoopla reports a -0.7% decline in house prices over the last three months.

Overall, house price movement in April was mixed, with sluggish growth observed in both directions, similar to March. It remains too early to predict how the rest of the year will play out.

House sales on par with 2019, as sellers proceed with caution

According to Rightmove's latest report, the number of agreed home sales has recovered to pre-pandemic levels, and is now only 1% behind the sales figures for March 2019.

However, despite this positive trend, homesellers are proceeding with caution. New sellers have only increased their prices by 0.2% (£890) this month, which is significantly lower than the expected average increase of 1.2% at this time of year. This suggests that most homesellers are heeding the advice of their estate agents and pricing their properties in line with the economy.

First time buyers face record properties

Despite the challenging economic climate, first-time buyers are confronting the most expensive property market yet. According to Rightmove, the average price of a two-bedroom or smaller property, commonly sought after by first-time buyers, has reached a record high of £224,963.

However, it’s first-time buyers who are primarily driving the market's recovery. Agreed sale figures in this sector were 4% higher in April 2023 than in March 2019, while sales for second-steppers and top-of-the-ladder steppers lagged behind at 4% and 3%, respectively.

The relentless growth of house prices over the last three years has made it increasingly difficult for first-time buyers to purchase a home, requiring larger deposits and higher household incomes. Nevertheless, demand for properties among these buyers remains high, as homebuying still appears to be a more worthwhile investment than renting in the long run.

Around 700,000 households missed rent or mortgage payments

One of the biggest stories on mortgages last month came from Which?, with the consumer body reporting that an estimated 700,000 UK households missed or defaulted on rent or mortgage payments. Which? noted that missed payments were particularly high among those renting, with one in twenty of the tenants surveyed affected.

In other news, the average first-time buyer mortgage rate for a five-year, 15% deposit mortgage has fallen to 4.46%. Zoopla has identified that some first-time buyers are taking out longer-term mortgages to combat current pressures on affordability, and purchasing cheaper, lower cost properties.

Get a house valuation from an expert!

House prices have skyrocketed over the past three years - but we’re now transitioning into a buyer’s market, with repricing now regular across the country. As a result, homeowners have a limited amount of time to reap the profits of the pandemic boom.

If you’re interested in finding out how much you’re sitting on, the best thing you can do is receive a valuation from a market professional. Estate agents are the best at evaluating properties, but as with any product or service, some are more effective than others.

Don’t have the time to compare them? Not a problem - our Estate Agent Comparison Tool does it all for you, ranking the best local agents by experience, speed, and percentage of asking price achieved. Did we mention it’s free?

Don’t let me down…

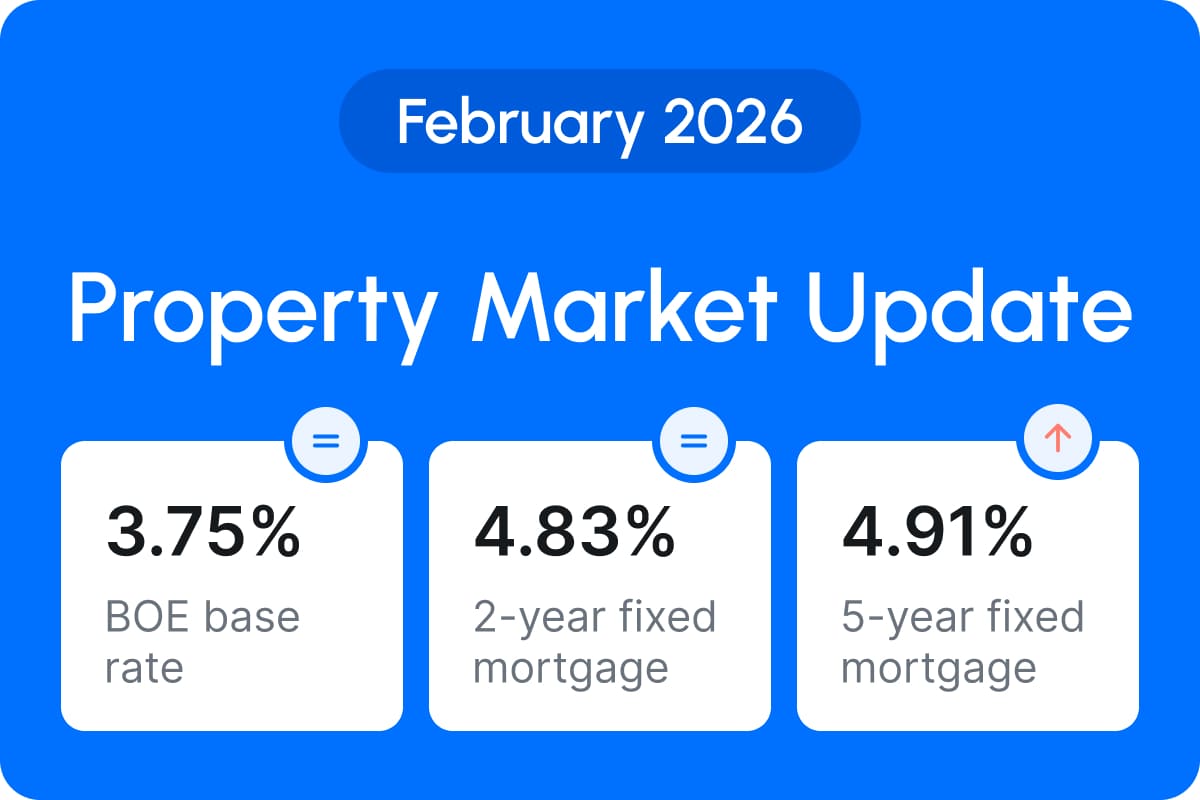

With the Bank of England’s interest rate set to rise (to 4.5%) for a 12th consecutive time, you’d be forgiven for thinking that we’re living in precarious times. However, things are expected to get easier, with no further hikes expected, and mortgages to remain fairly settled.

In the meantime, you can keep track of your most valuable asset with GetAgent’s Online House Valuation Tool, and stay up to date on the latest property news.

Thanks for reading, we’ll see you next time!

How much

is your home worth?

It’s always worth knowing the value of your home. Discover the price of your property with an instant valuation. GetAgent tracks the figures, so you don’t have to.

How much

is your home worth?

It’s always worth knowing the value of your home. Discover the price of your property with an instant valuation. GetAgent tracks the figures, so you don’t have to.

Compare estate agents

It takes 2 minutes.

Get in touch

020 3608 6556

Our lines are closed

We are a company registered in England & Wales, company number 09428979.

Copyright © 2026 GetAgent Limited