- Compare agents

- Online valuation

- Explore my area

- Home toolkit

- News & guides

- Estate agents by area

- Sold house prices by area

- Estate Agent ValuationRequest an in-person valuation with an agent to discover your property's true market value.

- Online Valuation ToolGet a free instant estimate of your home's value.

- EPC CheckerFind out if your home has a valid Energy Performance Certificate.

- Listing MonitorAlready on the market? See how your online property advert is performing.

- Selling guides

- Estate agent guides

- Mortgage advice

- Conveyancing guides

- Property news See All News & Guides

Agent shortlist

HouseWorth

Estimated reading time: 8 minutes

Welcome to the latest edition of the GetAgent Property Market Update! We’ve gathered insights from top experts across the UK to give you a well-rounded view of current market trends.

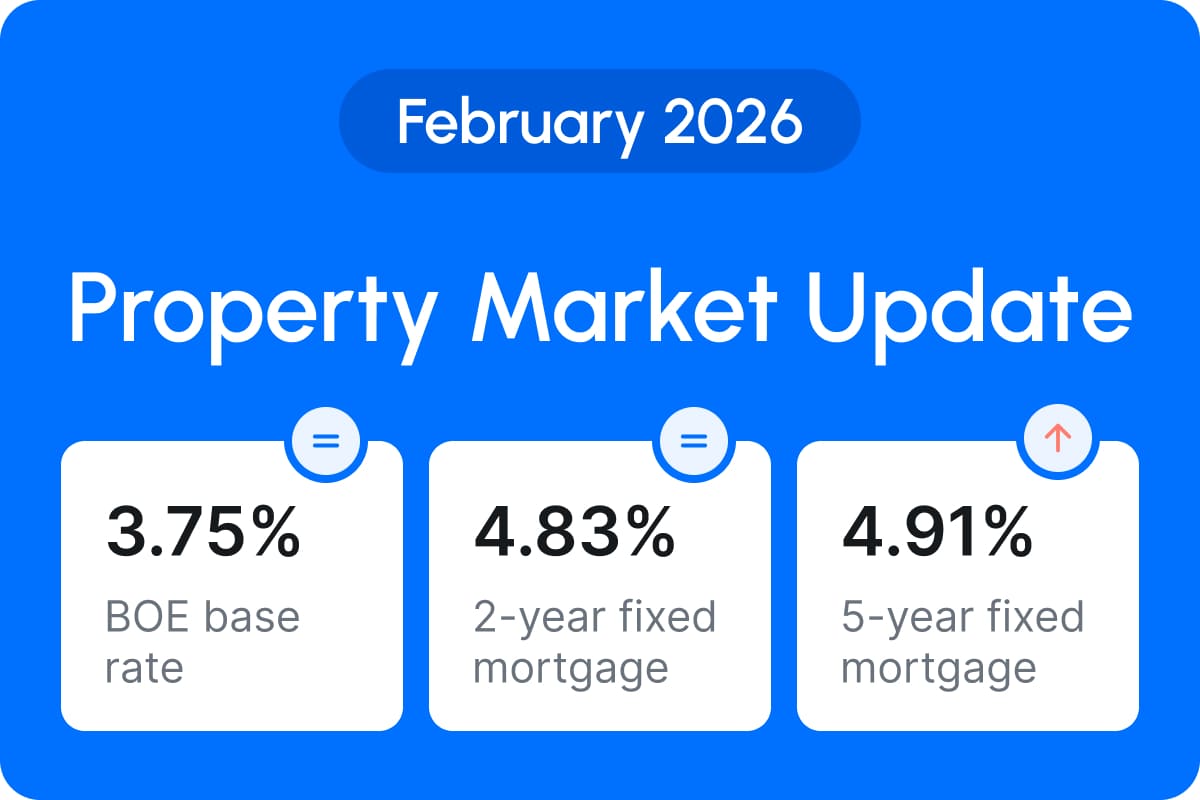

Since September 22nd, 2022, the Bank of England (BOE) has implemented over seven base rate increases. In June, the base rate experienced its most substantial jump since the previous year, rising from 4.5% to 5%. This raises an important question: will these measures be sufficient to rein in the rate of inflation? Why has core inflation proven to be remarkably resistant to the consecutive rate hikes by the Bank of England?

UK house prices have once again made the headlines, with Halifax reporting the biggest annual fall since 2011. This may sound like déjà vu to some of our readers, and you wouldn't be wrong. Last month, Nationwide made the headlines with a very similar story. While one cannot predict the future, especially with something as unpredictable as the property market, one thing is certain: the market is experiencing a repricing.

Let's dive into the latest market update.

Food inflation slows but core inflation remains stubborn

As mentioned earlier, the BOE increased its base rate to 5% on the 22nd of June. With markets now forecasting a peak in Bank Rate of over 6%, we can expect this to happen in the quarters ahead.

But what does this mean for the average homeowner? Helen Dickinson, OBE and Chief Executive of the British Retail Consortium indicates that consumer price inflation may be responding to the BOE’s intervention. “Food inflation slowed for the second consecutive month, particularly for fresh products, as retailers cut the price of many staples including milk, cheese and eggs…If the current situation continues, food inflation could drop to single digits later this year.” She adds, “However, it is imperative that (the) Government does not hamper this progress by introducing costly new policies.”

It's important to note that slowing inflation does not necessarily translate to falling prices. Rather, it indicates a decrease in the rate at which prices are rising. While we may not experience significant changes until 2024, there is optimism among experts that food prices will begin to decline in the first half of the year. However, prospective homeowners will still face challenges during this period due to steep rent hikes and persistently high inflation rates, making it difficult to save for house deposits.

Why is inflation not going down?

Inflation’s stubbornness can be attributed to several key factors. One such factor is our position as the third-largest net importer of food and drink, trailing only China and Japan (as reported by the Food and Agriculture Organisation of the United Nations). A combination of adverse weather conditions, geopolitical challenges like the Ukraine war, and certain oversights on the part of the BOE has left Britain particularly vulnerable to high food inflation.

Our country also relies heavily on natural gas imports for electricity generation. With Russia being one of the world’s largest exporters of natural gas, our energy prices have been greatly impacted by the war in Ukraine. Until wholesale prices come down, or our reliance on natural gas shifts, we are particularly vulnerable to this cause of inflation.

Halifax: House prices experience biggest annual fall since 2011

Halifax made headlines with their reports that annual house price growth had fallen to -2.6% in June from -1.1% in May. The typical UK home is now worth £285,932 versus a peak of £293,992 last August. House prices also saw a third consecutive monthly fall, down £300 from May.

Kim Kinnaird, Director of Halifax Mortgages views this annual decline as somewhat inevitable when viewed alongside the pandemic boom. "With very little movement in house prices over recent months, this rate of decline largely reflects the impact of historically high house prices last summer – annual growth peaked at +12.5% in June 2022 – supported by the temporary Stamp Duty cut."

Kinnaird is keen to point out that the annual growth figure does not tell the full story, with house prices doing better than expected despite Government mishaps. "To some extent, the annual growth figure also masks the fluctuations we’ve seen in the market over the past 12 months. Average house prices are actually up by +1.5% (£4,000) so far this year, with most of that growth coming in the first quarter, following the sharp fall in prices we saw at the end of last year in the aftermath of the mini-budget."

While annual house price growth is down, there have been pockets of growth across the UK. Zoopla reports that among the top ten regions experiencing growth, Derby (East Midlands), Wolverhampton (West Midlands), Dorchester (South East), Wakefield and Huddersfield (Yorkshire & The Humber), are some of the highest.

But why are house prices increasing in these particular areas?

As cost-of-living pressures intensify, prospective buyers are seeking more affordable properties. The larger homes that became popular during the pandemic boom are now seeing decline, whereas smaller properties, like terraced and semi-detached properties, are retaining their values - and in some cases, exceeding them.

The value in knowing your home's value

In today’s market, buyers have the luxury of taking their time and revisiting properties for a second viewing. As a result, motivated homesellers need to approach the market sensibly and price their homes in alignment with the conditions of their local market.

Although there’s an increase in available properties for sale, demand still outweighs supply. Exceptional homes that stand out from the crowd continue to attract a significant number of prospective buyers.

Sellers who accurately price their properties are experiencing considerable success in this market. Get a free estimate with GetAgent’s instant valuation tool, My Property Tracker. Give it a go today.

Asking prices fall for first time in June since 2017

According to Rightmove, average asking prices experienced their first decline in June since 2017. Although the decrease (£82) was not substantial, it indicates a significant shift in selling strategies, especially when compared to the market boom observed from 2021 to 2022. In the past, sellers were able to achieve up to 120% of their property's asking price. Today, they are adopting a more cautious approach based on advice from local estate agents.

While it’s typical for asking prices to continue falling in accordance with the seasonal pattern, Rightmove still projects a 2% annual decrease in new seller average asking prices by the end of 2023.

Government announces Mortgage Charter amid market tension

On the 26th June, the Government announced a new Mortgage Charter which sets out the standards signatories will adopt when helping their customers with mortgage problems. Over 90% of lenders operating in the UK have signed the charter, with signatories agreeing to a number of standards designed to reassure borrowers. Some of these include:

- Borrowers can’t be forced to leave their home without consent, unless in exceptional circumstances, in less than a year from their first missed payment.

- Customers approaching the end of a fixed rate deal have the chance to lock in a deal up to six months ahead. They’ll also be able to manage their new deal and request a better deal with their lender right up until the start of their new term.

- Borrowers who are up to date with their repayments may switch to interest-only payments for six months or extend their mortgage term to reduce their monthly payments, with the option to revert to the original term within 6 months by contacting the lender.

The charter has arrived at an opportune time, although it is still too early to determine whether it will adequately assist vulnerable borrowers. Nationwide has reported that a significant number of borrowers, approximately 400,000 each quarter, are expected to refinance their mortgages. By the end of 2023, around 20% of the fixed-rate mortgage stock is expected to be refinanced, increasing to 40% by the end of 2024.

These borrowers will likely face significantly higher payments compared to their original contract agreements. For instance, the average rate for a 5-year fixed 85% loan-to-value (LTV) mortgage has risen from 4.56% to 5.2% within a span of four weeks.

While homeowners are generally stress-tested to withstand such scenarios, the impact is nevertheless discomforting. According to Rightmove's data, there is currently no discernible effect on buyer demand, but there is a slight decrease in sales activity, resulting in slower property sales.

(For full Mortgage Charter information, refer to the Gov.UK website)

Summary: Under pressure!

It’s likely that mortgage rates will get even higher before year’s end. If you’re looking to remortgage soon, check out our quick guide to fixing mortgages. And, if you haven’t already, check out the Mortgage Charter for more information on how lenders can better help you.

As always, thanks for reading, we’ll see you next time.

How much

is your home worth?

It’s always worth knowing the value of your home. Discover the price of your property with an instant valuation. GetAgent tracks the figures, so you don’t have to.

How much

is your home worth?

It’s always worth knowing the value of your home. Discover the price of your property with an instant valuation. GetAgent tracks the figures, so you don’t have to.

Compare estate agents

It takes 2 minutes.

Get in touch

020 3608 6556

Our lines are closed

We are a company registered in England & Wales, company number 09428979.

Copyright © 2026 GetAgent Limited