- Compare agents

- Online valuation

- Explore my area

- Home toolkit

- News & guides

- Estate agents by area

- Sold house prices by area

- Estate Agent ValuationRequest an in-person valuation with an agent to discover your property's true market value.

- Online Valuation ToolGet a free instant estimate of your home's value.

- EPC CheckerFind out if your home has a valid Energy Performance Certificate.

- Listing MonitorAlready on the market? See how your online property advert is performing.

- Selling guides

- Estate agent guides

- Mortgage advice

- Conveyancing guides

- Property news See All News & Guides

Agent shortlist

HouseWorth

Property news09 November 2023

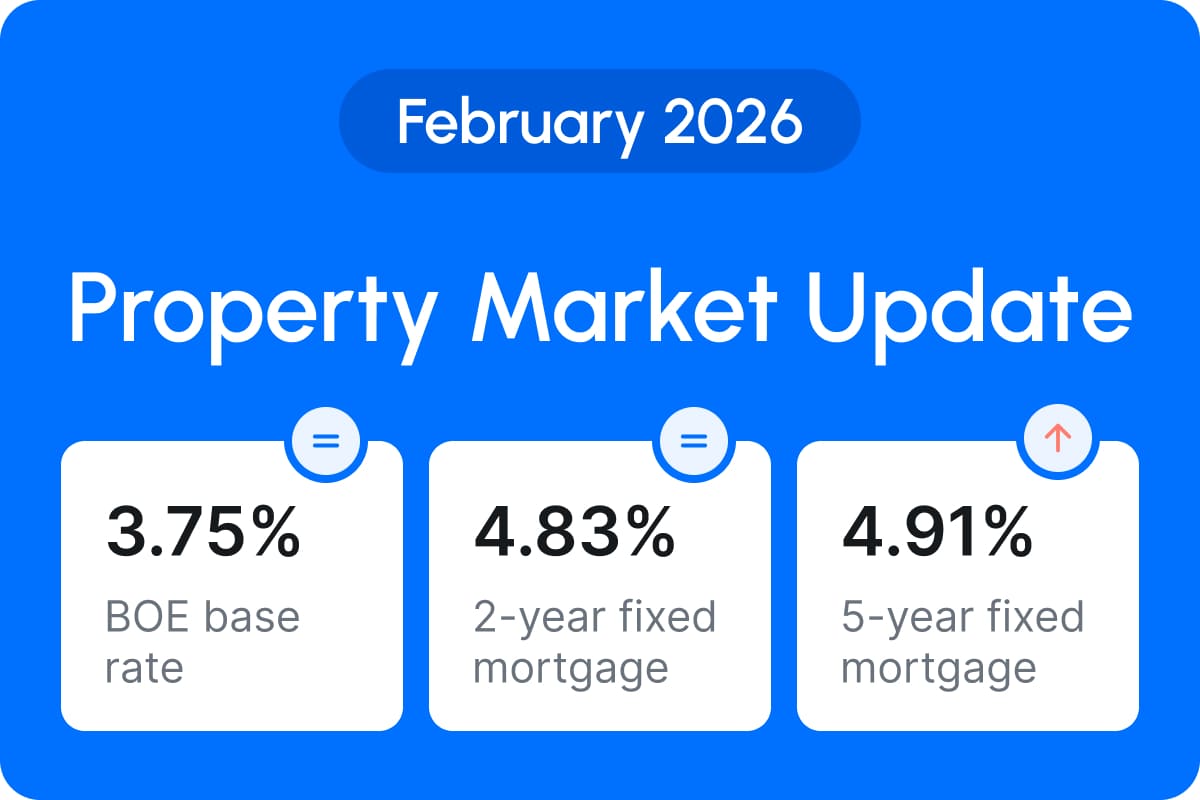

Property Market Update: October 2023

Sam Edwards

Content Marketing Manager

Estimated reading time: 6 minutes

Welcome to the October edition of the Property Market Update! We've collaborated with top experts from across the UK to provide you with a comprehensive view of the latest news from the market.

This month, a noteworthy trend is emerging as mortgage lenders engage in intense competition. The question on everyone's mind is whether these new low-interest packages are genuinely beneficial.

In a twist, house prices have experienced an unexpected bump, with Nationwide and Halifax both reporting an increase. What does this mean for the overall market outlook?

House prices experience a bump - but don’t get too excited…

According to Nationwide's recent report, average national house prices registered a 0.9% increase in October. This 'positive' development also contributed to an improved annual house price growth rate of -3.3%, up from -5.3% in September.

Unfortunately, the overall housing market isn't undergoing a revival. In September, only 43,000 mortgages were approved for property purchases, a figure significantly below the monthly average in 2019, indicating a market that remains relatively weak for this time of year. Additionally, Zoopla's latest market update highlights that buyer demand in October is 25% lower than the five-year average.

So, what's behind the rise in house prices?

One key factor is the limited housing stock and the comparatively high values of properties currently available in the market. This means that those with the financial capacity to make higher down payments are currently in a better position to benefit from lower interest rates. Moreover, there is little evidence of forced selling, which typically exerts downward pressure on house prices, and mortgage arrears are at a low.

The Bank of England's base rate remains unchanged, and inflation rates are running lower than the growth in average earnings. These are positive signs for the economy, but their impact has yet to reach the majority of individuals. While the burden of the cost of living is said to be easing, homeowners and renters have yet to experience substantial relief. As a result, consumer confidence remains subdued, and potential buyers are adopting a cautious approach.

Lenders adjust interest rates for existing borrowers, but there’s a catch…

In recent months, the mortgage market has regained stability, leading to increased competition among lenders. Similar to what we saw in August, where major banks and building societies reduced interest rates on their fixed products, we're now witnessing the emergence of some new and seemingly improved offers.

Early in October, Skipton Building Society introduced new products designed to assist borrowers facing repayment challenges. They unveiled two-year fixed loans starting at an attractive 3.35%, exclusively tailored for existing borrowers. These rates stand out in today's market, where the average two-year fixed rate hovers at 5.4%.

However, there's a significant trade-off. Unlike most mortgage products, which come with a fixed product fee ranging from several hundred pounds to a thousand, these loans bear a hefty 5% product fee that must be paid upfront or added to the total debt. For many homeowners, this represents a substantial financial commitment.

Virgin Money has followed suit, recently introducing a two-year fixed rate at 5.09% with an 1% product fee on October 27th.

Unless you have substantial savings or are comfortable adding 1 - 5% to your overall loan, it's advisable to seek guidance from a mortgage broker to determine the best course of action. It's important to keep in mind that a two-year fixed term is relatively short, and any additional debt can impact your future interest rates once the fixed term concludes.

If you're planning to move to a new home in the coming months, securing a mortgage agreement in principle is vital. While it’s always a prudent step, in today's economic climate, it's more critical than ever. Determine whether your bank is willing to extend a loan to you before delving into the homebuying process to avoid any uncomfortable surprises down the road.

Looking ahead: Cloudy with a chance of price falls

Experts are in agreement that, excluding this extraordinary month, the foreseeable trend for house prices points toward a continued decline well into 2024, with 2025 potentially marking a turning point for growth. Kim Kinnaird, Director of Mortgages at Halifax, emphasises that the present decrease in prices is a temporary anomaly in the broader context of a generally upward trajectory:

“Across the medium-term, with financial markets not anticipating a decline in the Bank of England’s Base Rate soon, we expect house prices to fall further overall – with a return to growth from 2025. (…)The current picture should continue to be seen in the context of the longer-term house price trend as, on average, prices remain around £40,000 above pre-pandemic levels.”

The Bank of England anticipates a sustained decrease in inflation. Given the sequence of adjustments to the base rate throughout this year, the full impact on inflation is projected to materialise approximately two years from now. Presently, inflation stands at 6.7%, with expectations of a return to around 2% in the first half of 2025.

If this projection holds, there's potential for mortgage rates to decline more rapidly in 2024 than initially anticipated, potentially leading to increased mortgage applications and higher property sales numbers. Currently, banks are subjecting applicants to stress tests based on rates between 8-9%, despite actual rates being closer to 5%. This, in turn, has contributed to the decrease in the number of property sales.

Some advice to sellers

Rightmove provided some useful stats in their monthly index:

- The number of buyers enquiring at each available home is 8% higher than 2019’s more stable market.

- If your property receives an enquiry on the first day of marketing, it’s 60% more likely to find a buyer.

If you want to take advantage of the extra buyers and receive an inquiry on your home’s first day of marketing, it’s clear that pricing it right from the outset is essential.

With unparalleled knowledge about your local market and a vested interest in your success, the best agents know how to accurately price a home.

Compare with GetAgent and rank local agents according to experience, speed, and percentage of asking price achieved. It’s the smart thing to do!

It takes 2 minutes.

Summary: Keep your chin up!

As we hurtle towards another new year, it's a good time to look back at our journey so far. We've experienced quite a ride, from last year's budget, to the endless bumps to the Bank of England's base rate, and the fast transition to a buyer's market.

Looking ahead, we hope for a smoother and more predictable path. Thank you for reading, and we'll be back with the November update next month!

How much

is your home worth?

It’s always worth knowing the value of your home. Discover the price of your property with an instant valuation. GetAgent tracks the figures, so you don’t have to.

How much

is your home worth?

It’s always worth knowing the value of your home. Discover the price of your property with an instant valuation. GetAgent tracks the figures, so you don’t have to.

Compare estate agents

It takes 2 minutes.

Get in touch

020 3608 6556

Our lines are closed

We are a company registered in England & Wales, company number 09428979.

Copyright © 2026 GetAgent Limited