- Compare agents

- Online valuation

- Explore my area

- Home toolkit

- News & guides

- Estate agents by area

- Sold house prices by area

- Estate Agent ValuationRequest an in-person valuation with an agent to discover your property's true market value.

- Online Valuation ToolGet a free instant estimate of your home's value.

- EPC CheckerFind out if your home has a valid Energy Performance Certificate.

- Listing MonitorAlready on the market? See how your online property advert is performing.

- Selling guides

- Estate agent guides

- Mortgage advice

- Conveyancing guides

- Property news See All News & Guides

Agent shortlist

HouseWorth

Property news12 March 2020

How will low interest rates impact moving house?

Rosie Hamilton

Writer & Researcher

Estimated reading time: 4 minutes

Table of contents

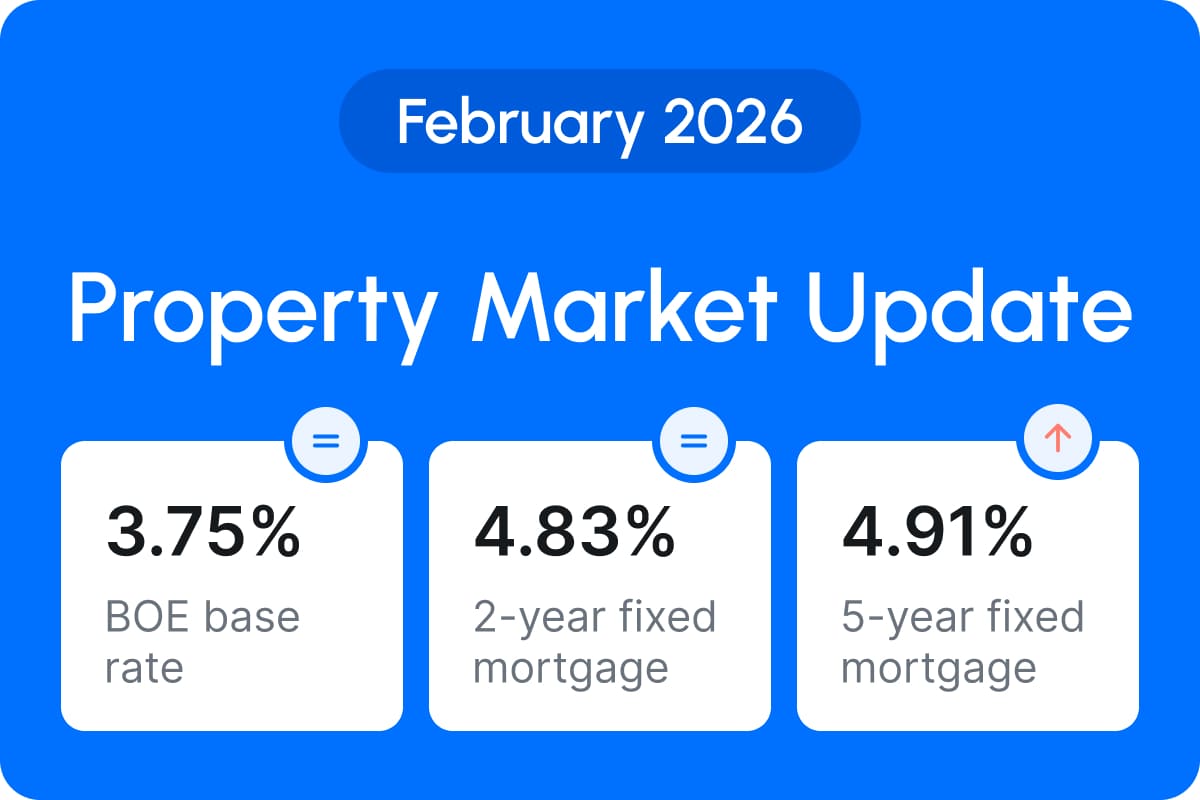

Update: On March 19th 2020 the Bank of England again reduced rates from 0.25% to 0.1%

On March 11th 2020 the Bank of England announced an emergency cut to its interest rate as a defense measure against the economic impact of coronavirus. The rate was slashed from 0.75% to 0.25%. The only other time the base rate has been this low was in August 2016.

The base rate impacts all other interest rates. When the rate is low, it costs less to borrow money, but it makes saving money less appealing.

The measure is designed to protect businesses, particularly vulnerable small companies and startups. But it’s likely to also impact the housing market in ways that could be beneficial for your home sale.

What happens to the housing market when interest rates are reduced?

As a general rule lower interest rates encourage more home buyers to enter the market. Tracker and Standard Variable Rate mortgages and influenced by the interest rate set by the Bank of England. Tracker mortgages usually follow this rate directly. Standard Variable Mortgages follow an interest rate set by your lender, but these also tend to follow the Bank of England rate to remain competitive.

Because of this, the decrease to the Bank of England interest rate makes Tracker and Standard Variable Rate mortgages more affordable. So, more people are able to borrow the money they need to buy a house.

The knock on effect of this is that house prices tend to increase when interest rates are low, because there's greater demand in the market. This is particularly positive if you’re trying to sell your home. More buyers entering the market means you’re more likely to sell your home quickly and for a higher price.

Mortgages

Given that the decreased bank rate is likely to affect mortgage rates, this could be a good time to consider your own mortgage situation too.

If you’re coming to the end of your fixed rate or tracker mortgage, think about moving to a new deal. It’s likely that any fixed rate mortgage you switch to will now have a cheaper rate. You can look into remortgaging up to 6 months before your introductory period ends.

Low interest rates could make overpaying your mortgage a good option too. Overpaying when interest rates are low means that when they increase in the future, you'll only have to pay the higher rates on a smaller amount. However, if you have any other debts, it can make sense to pay them off first because they are likely to have much higher interest rates.

Check out our handy guide for more information on the different types of mortgages and how they work.

If you're unsure what the best course of action is for your mortgage, make sure to get advice from an independent financial adviser.

How Coronavirus complicates the situation

Of course, because the interest rate decrease is in response to coronavirus, it’s important to take into account the impact that this outbreak could have.

The last time there was a major outbreak in the UK was with Swine Flu in 2009. During this time there was a reduction in the number of mortgages approved and a decrease in construction activity. This had an impact on the number of buyers entering the market, but because the supply of new housing was low house prices remained more stable than expected.

On the other hand, if this interest rate cut is a temporary measure, some mortgage rates will see no change. Lenders might decide to maintain the current rates on their Standard Variable Rate mortgages, rather than reducing them. The best thing you can do is to check with your mortgage provider to see whether the changes will affect you.

New buyers will still be able to access lower mortgage rates, and this should protect the housing market, even if there is a dampening in demand. Forbes suggests that the impact of reduced interest rate should support stable house prices, meaning you do not need to worry too much about house prices falling in response to the outbreak.

Thinking about

selling your home?

Picking the right estate agent is vital for a successful sale. GetAgent makes choosing simple. Discover the best performing agents in your area.

- Free

- Data-driven

- No obligation

Thinking about

selling your home?

Picking the right estate agent is vital for a successful sale. GetAgent makes choosing simple. Discover the best performing agents in your area.

- Free

- Data-driven

- No obligation

Compare estate agents

It takes 2 minutes.

Get in touch

020 3608 6556

Our lines are closed

We are a company registered in England & Wales, company number 09428979.

Copyright © 2026 GetAgent Limited